Table of Contents

What to Consider When Applying for a Bridging Loan?

Applying for a bridging loan can be a strategic move for those needing short-term financing solutions, but it’s crucial to weigh several factors before making a decision.

During property transactions, renovation projects, or urgent business needs, these loans can fill financial gaps. However, understanding the terms, interest rates, and repayment schedules is vital to avoid potential pitfalls. It is possible to estimate costs and plan effectively by using a bridging loan calculator.

A bridging loan application that is prepared properly can significantly increase your chances of being approved.

A bridging loan can help you bridge the gap between two financial situations, and this article examines the essential considerations, including pros and cons, lender requirements, and strategies for making the application process go smoothly.

Take a closer look at bridging loans to learn how to navigate the complexities of them and make informed decisions.

Understanding UK Bridging Loans

If you’re looking for short-term financing, understanding bridging loans is crucial. The following are three key aspects to consider:

- Definition & Purpose: Bridging loans are short-term loans used to bridge the gap between the sale of one asset and the purchase of another. They are usually used in property transactions, allowing buyers to secure a new property before selling their current one.

How Bridging Loans Work: Bridging loans are secured by property, and the amount borrowed is typically a percentage of the property’s value. Due to the short-term nature and risk involved, short-term mortgages can carry higher interest rates. Typically, the repayment is structured as a lump sum.

Types of Bridging Loans: Open and closed bridging loans are the two main types of bridging loans in the UK. The open bridging loan has no fixed repayment date, making it flexible, but potentially more expensive. Closed bridging loans have a fixed repayment date, which is usually aligned with the completion of a property sale.

Webinar Recording: how to obtain a bridging loan using the Lendlord platform

How a Bridging Loan Can Bridge Your Financial Gap

Bridging loans can help you navigate temporary cash flow challenges with an effective short term financial solution.

Loans like these are especially useful for individuals and businesses who need quick access to funds during transitional periods, such as buying a new property before selling an old one. With bridging loans, you can seize time-sensitive opportunities without delay by receiving rapid financing.

It is important to understand the loan’s terms and conditions in order to make sure it aligns with your financial goals. Understanding how bridging loans fit into your broader financial planning can help you make informed decisions.

Analyzing Bridging Loans' Function and Impact

Bridge loans are essential during times of transition, especially for those seeking short-term financial support.

As an example, they can be used to facilitate the purchase of a new property while you wait for the sale of your existing property.

Individuals and businesses can leverage these loans to leverage opportunities that require immediate funding, which has a significant impact. However, analyzing their function requires an understanding of interest rates, terms, and potential risks.

Considering these factors can help borrowers make well-informed choices based on their financial strategies, in order to make well-informed decisions.

Which Bridging Loan Is Right for You?

Understanding the different types of bridging loans available and how they align with your financial needs is key to selecting the right loan.

For those awaiting uncertain funds, open bridging loans offer flexibility with no fixed repayment date. A closed bridging loan, on the other hand, has a fixed payment date, making it an attractive option for borrowers that have a clear exit strategy.

Choosing the right loan type depends on your financial situation, timeline, and investment type. By exploring these options in depth, you will be able to match the appropriate loan with your financial goals, ensuring that this powerful financial tool is used effectively.

Critical Considerations for Bridging Loans Borrowers

When applying for a bridging loan, it’s important to consider several key factors to ensure it meets your financial needs and capabilities. Here are three critical considerations:

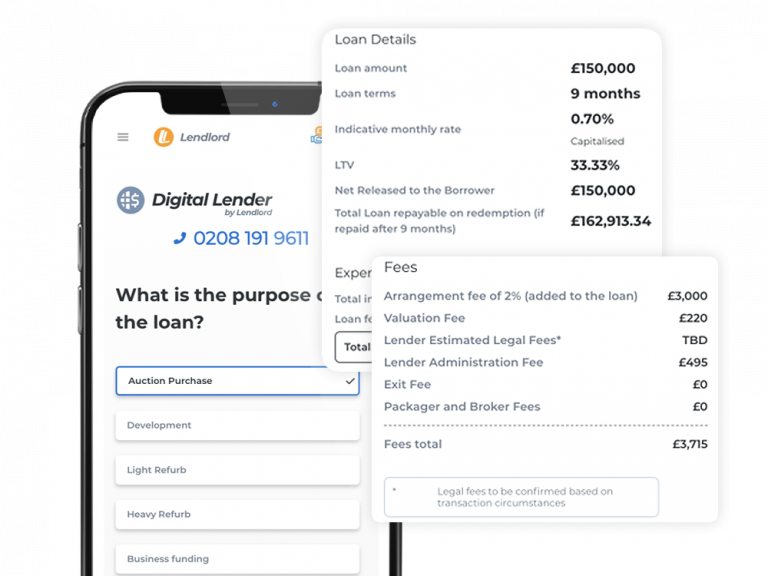

Interest Rates and Fees: Bridging loans typically come with higher interest rates compared to traditional mortgages due to their short-term nature and associated risk. It’s essential to compare rates from different lenders and understand any additional fees, such as arrangement or exit fees, that may impact the overall cost.

Loan Terms and Repayment Schedules: Bridging loans are meant to be short-term solutions, often ranging from a few weeks to 12 months. It’s crucial to have a clear plan for repayment, whether through the sale of an asset, securing long-term financing, or another exit strategy. Ensure the loan term aligns with your financial timeline.

Eligibility and Application Process: Lenders will assess your financial situation, credit history, and the value of the asset being used as security. Preparing a strong application with necessary documentation, including proof of income and an exit strategy, can increase your chances of approval and favorable terms.

The True Price of Bridging Loans: A Guide to Interest Rates and Fees

The true price of bridging loans extends beyond interest rates, encompassing various fees that can significantly impact the overall cost.

Due to the short-term nature of these loans, the interest rates are generally higher, but borrowers must also consider arrangement fees, exit fees, and legal fees, which can add up quickly.

Evaluating the total expense requires understanding how these elements interact. The analysis of these costs in detail reveals the true financial commitment involved and the need for thorough financial planning to ensure the loan serves its intended purpose without unexpected financial strain.

Bridging Loan Terms and Repayment Schedules: An Overview

Bridging loan terms and repayment schedules are designed to provide short-term financing solutions, typically ranging from a few weeks to 12 months.

While these loans are flexible, a clear exit strategy is necessary to ensure timely repayment, such as the sale of the property or refinancing. There can be significant differences in terms between borrowers and lenders depending on their financial profiles.

Understanding the intricacies of these terms is essential for aligning the loan with your financial goals. Exploring the nuances of bridging loan agreements reveals how they can fit into broader investment strategies and address specific funding needs.

The process of eligibility and application

Bridging loans require careful preparation during the process of eligibility and application. Borrowers are typically evaluated on the basis of their creditworthiness, financial stability, and the value of the property being used as collateral.

Having a well-documented financial history and a clear exit strategy can enhance your chances of approval. The application process may include submitting detailed financial statements, proof of income, and a comprehensive repayment plan.

A successful application requires an understanding of these requirements. Understanding the specifics of this process can help you prepare and present your application effectively to lenders.

Making the Most of Your Bridging Loan

To maximize the benefits of your bridging loan, strategic planning and careful execution are key. Here are three essential strategies:

Define a Clear Exit Strategy: Before taking out a bridging loan, ensure you have a well-defined exit strategy. This could involve selling a property, refinancing, or securing long-term financing. Having a clear plan for repayment not only helps you avoid financial strain but also makes your application more attractive to lenders.

Understand the Costs Involved: Use a bridging loan calculator to accurately estimate the total cost, including interest rates and fees. Being aware of the full financial commitment allows you to plan your budget effectively and ensure the loan is affordable within your broader financial plan.

Stay in Communication with Your Lender: Regular communication with your lender can help you address any potential issues early on. Be proactive in discussing any changes in your financial situation or project timeline to avoid complications and ensure a smooth loan experience.

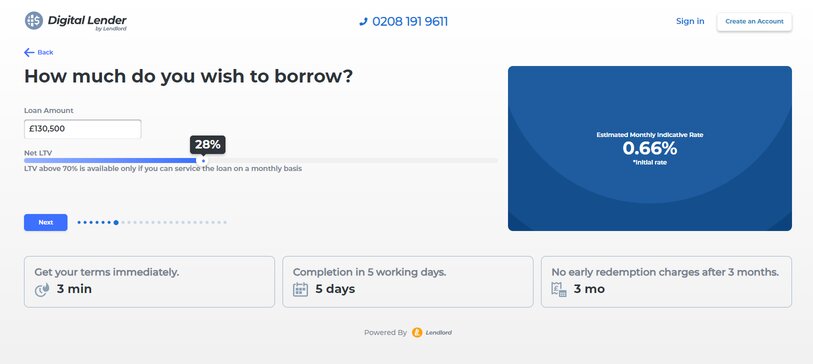

Calculating The Amount of a Bridge Loan Using a Bridge Loan Calculator

Understanding your financial options requires understanding the amount of a bridge loan using a bridging loan calculator.

Using this tool, you can estimate the total amount of a loan based on factors such as the property value, existing mortgage balance, and potential fees.

The calculator can provide insights into monthly interest payments and overall costs by inputting these details. This calculator can clarify the financial implications of taking out a bridge loan and assist you in planning your repayment strategy.

When you examine these calculations in depth, you will be able to determine how to align the loan with your financial goals.

Tips for a Successful Bridge Loan Application

Submitting a successful bridge loan application requires strategic preparation and attention to detail. You should compile comprehensive documentation that proves your financial stability, including proof of income, credit history, and collateral value.

Be clear about your exit strategy so that the lender knows how you plan to pay back the loan. Additionally, maintain accurate and current information to avoid delays or rejections. Engaging with lenders early and understanding their specific requirements can significantly enhance your application’s success.

The more you refine these elements, the more likely you will be to secure the funding you need.

Avoid These Common Mistakes When Applying for a Bridging Loan

You should avoid common mistakes when applying for a bridging loan to avoid financial setbacks. Unexpected expenses can arise when you overlook hidden fees and interest rates.

Failure to establish an exit strategy may lead to financial strain and difficulties repaying the loan. It’s also possible to enter into an unfavorable agreement if you don’t fully understand the loan terms and conditions.

To avoid these pitfalls, make sure your application is thorough and accurate, with all necessary documentation. Understanding these common errors can help you navigate the application process more effectively.

Questions and Answers

The first step is to assess your financial needs and determine if a bridging loan is the right solution for your situation. Consider the purpose of the loan, the amount needed, and the repayment timeline.

Having a clear exit strategy is crucial. It outlines how you plan to repay the loan, whether through property sale, refinancing, or other means, and ensures you can meet repayment obligations.

Consider both the interest rate and any additional fees, such as arrangement or exit fees. Understanding the total cost of the loan helps you compare offers and choose the most cost-effective option

A bridging loan calculator helps estimate the total loan cost, including interest and fees, allowing you to assess affordability and plan your budget effectively.

Documentation usually includes proof of income, credit history, details of the property being used as collateral, and a clear exit strategy.

Your credit history can impact the terms and approval of your loan. A strong credit history may lead to more favorable interest rates and conditions.

Common mistakes include not having a clear exit strategy, underestimating costs, and failing to understand loan terms fully. Avoid these to ensure a smooth application process.

Improve your chances by preparing a comprehensive application, providing accurate documentation, and clearly outlining your exit strategy to lenders.

Bridging loans can be open or closed. Choose based on your repayment timeline and financial situation—open loans offer more flexibility, while closed loans have a fixed repayment date.

Regular communication helps address any issues early, ensuring that both parties are aligned and that the loan process goes smoothly, minimizing potential misunderstandings.

Recap: What to Know Before Applying for a Bridging Loan

Applying for a bridging loan can be a smart financial move if you know what to consider. Understanding the types of bridging loans and calculating costs using a bridge loan calculator are key steps in the process.

Crafting a successful application means avoiding common mistakes like ignoring hidden fees or lacking a clear exit strategy. Ensure you prepare thorough documentation, demonstrate your financial stability, and maintain open communication with lenders.

Using bridging loans makes it possible to bridge financial gaps and seize opportunities by minimizing interest rates, fees, and repayment terms. Take advantage of these insights to become a savvy borrower!

Jamie York and Lendlord – How Technology Empowers Property Investors

Sign Up for Free Today & Get 40% Off Lendlord Premium Plan!