We have just published a new article on the Property Reporter: “The importance of your portfolio LTV”.

In this post we would like to show you how you can track your portfolio LTV using Lendlord.

What is an LTV and why does it matter to landlords?

LTV is all about how much your mortgage borrowing is in relation to how much your property is worth. It’s a percentage figure that reflects the proportion of your property that is mortgaged, and the equity that you hold within them.

For example, if you have a mortgage of £150,000 on a house that’s worth £200,000, you have a loan-to-value of 75% – therefore you have £50,000 as equity. Loan-to-value becomes a key consideration when buying or selling a property, remortgaging or releasing equity. This is a very rudimentary explanation but it’s a vital component which sometimes gets overlooked by some landlords.

LTV levels matter because this is what lenders base their lending decisions around. Specialist lenders will take a look at a landlords LTV level across their whole portfolio and base any decision around this information as this indicates present and future risk, plus outstanding liabilities.

Generally speaking, the lower the LTV across the portfolio, the more comfortable lenders will be about future lending, and this will usually be reflected on the kind of rates on offer. Lower LTVs will also help open the doors to capital raising opportunities which could be vital in uncertain times where opportunities will continue to present themselves.

We know that robust property management will reap rewards over the short, medium and longer terms, especially in a time where a tax and regulatory squeeze has been evident. Meaning that a stronger grasp of LTV’s and how much equity landlords have in individual properties and across their portfolios will prove an important base for better managing these properties.

Not to mention providing a perfect springboard for realising their borrowing and capital raising position to take advantage of a potentially hesitant property market which could well be laden with opportunities for savvy investors.

So how you can track your LTV using Lendlord?

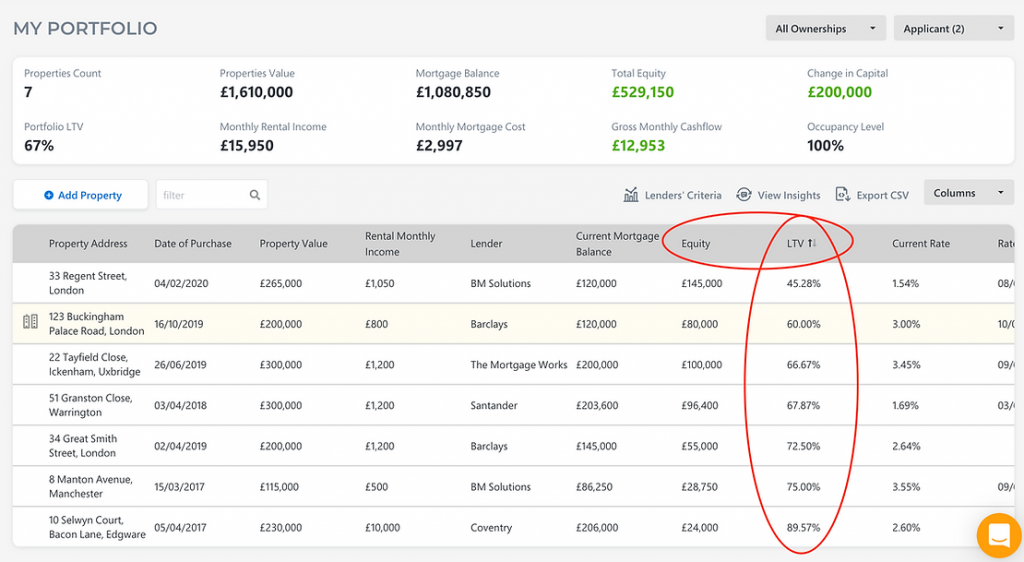

First, enter your properties details on My Portfolio page. You can track over 100 different data items but for calculating your LTV you just need to enter 2 main fields: Property Value (estimated) and your Current Mortgage Balance.

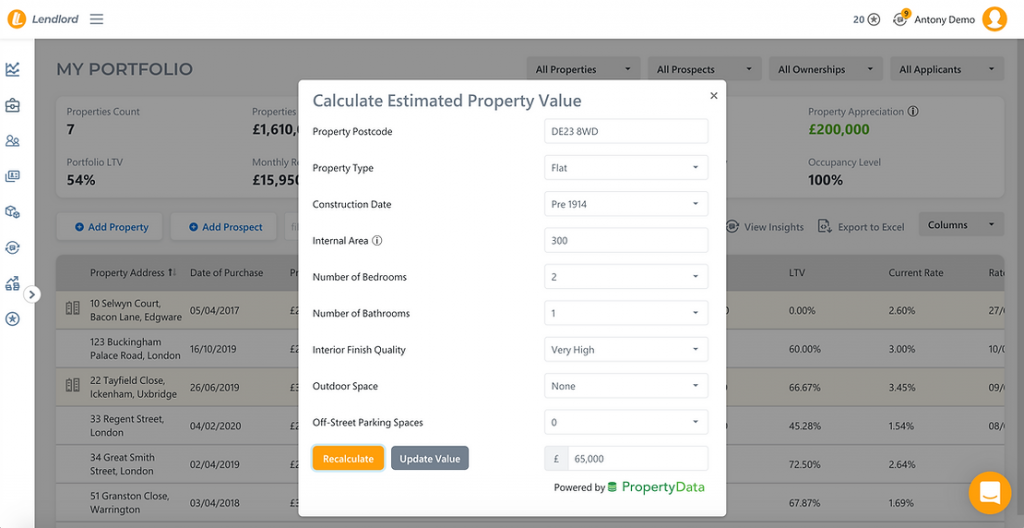

If you are not sure what is your property value, you can use our calculator that is using “Property Data” API to get indication on your current property price (please be noted that it’s just an estimation and might be not accurate. You can tweak and change the value anytime):

Track your current mortgage balance. If your mortgage payment method is “Capital and Interest” the platform will calculate the new balance every month (a new feature), so you will see the impact on your LTV.

After doing that, you will have the LTV calculated for each property and for the entire portfolio:

If you own some of your properties by a company, you can filter your portfolio and review your LTV under different segments. The next video explains how to do it:

https://youtube.com/watch?v=ONlVMl6WEx0%3Fautoplay%3D0%26mute%3D0%26controls%3D1%26start%3D30%26origin%3Dhttps%253A%252F%252Fwww.lendlord.io%26playsinline%3D1%26showinfo%3D0%26rel%3D0%26iv_load_policy%3D3%26modestbranding%3D1%26enablejsapi%3D1%26widgetid%3D1