Since the new buy to let portfolio stress tests were introduced in 2017, there has been a steady increase in the number of borrowers purchasing new buy to let property in limited companies.

The reason for this is that a limited company is viewed on its own merit and as a separate legal entity thereby allowing a lender to apply a lower stress test than would be applied were a mortgage application to be made in one’s sole name. For example, a higher rate taxpayer may face an interest cover ratio (ICR) stress test of 145% of the market rental calculated at an interest rate of 5.5%. Were this same application to be made by a limited company, the calculation would be lower at 125% of the market rental calculated at an interest rate of 5.5% or event a lower rate if applying for a five year fixed rate.

Not all lenders offer limited company mortgages but the number of lenders in this space are growing all the time.

Purchasing a property in a limited company name can have several advantages besides an improved stress test. If the landlord already owns under four buy to let properties in their sole name, they can still purchase a new property in a limited company name and continue to benefit from not being considered a portfolio landlord for the existing properties that are owned. This will allow for existing properties to be remortgaged using a non-portfolio landlord criteria potentially achieving more competitive products.

In all cases it is essential to take independent tax advice when considering whether to purchase in a personal name or limited company. A lower rate tax payer for example may not benefit as much from a limited company structure as the lender arrangement fees and interest rate are likely to be higher. Although this may be recouped by a higher rate taxpayer in paying less tax overall, a lower rate taxpayer will not necessarily face the same benefit.

Given the above, Lendlord is now enhancing its current limited company support to include the criteria of lenders who offer mortgages for limited companies and their mortgage/remortgage rates. This allows the platform to analyse your portfolio and suggest available rates from several lenders.

So how to get started:

1. Sign In or Sign Up Free

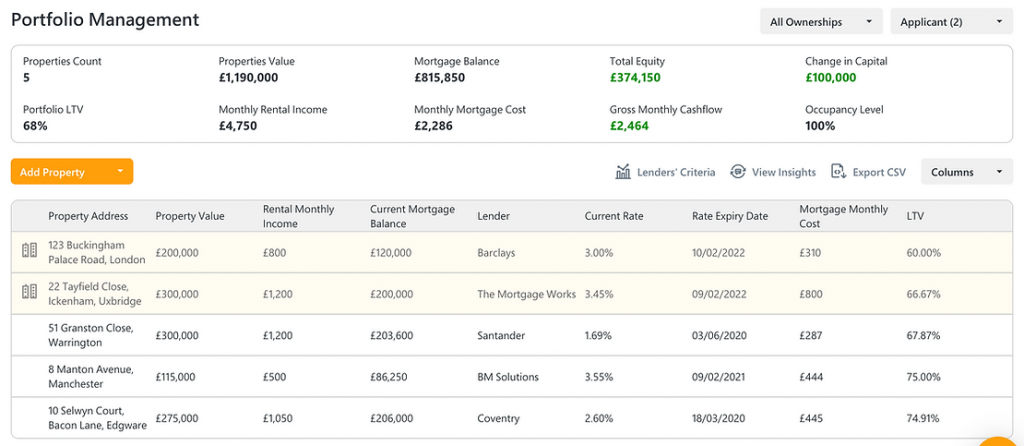

2. If you are a new user, please update your property details on “My Portfolio” page. Please make sure to pick the right ownership on each property (Private or Company):

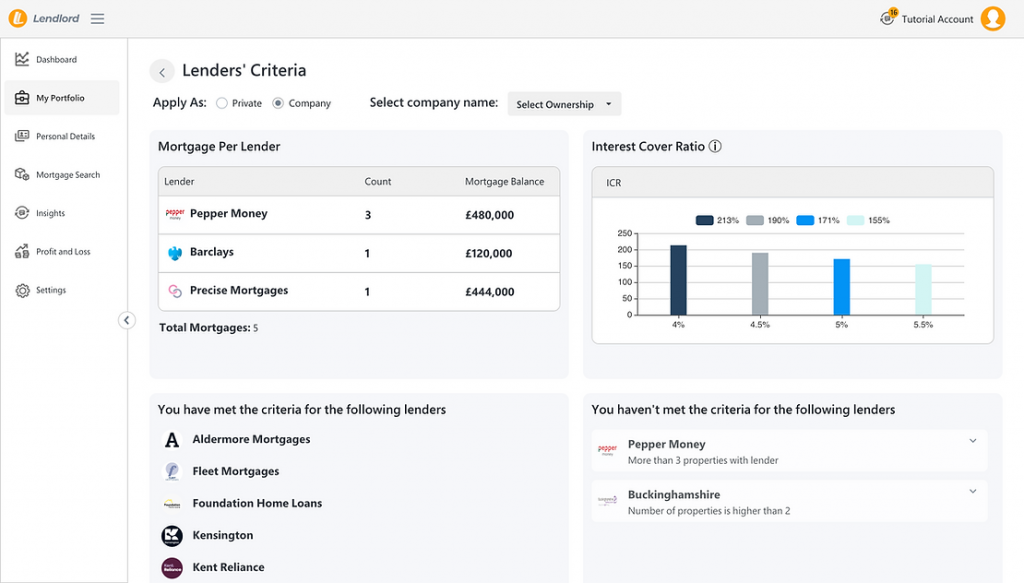

3. Click on “Lenders’ Criteria” and get the lenders that are available for your new mortgage or remortgage:

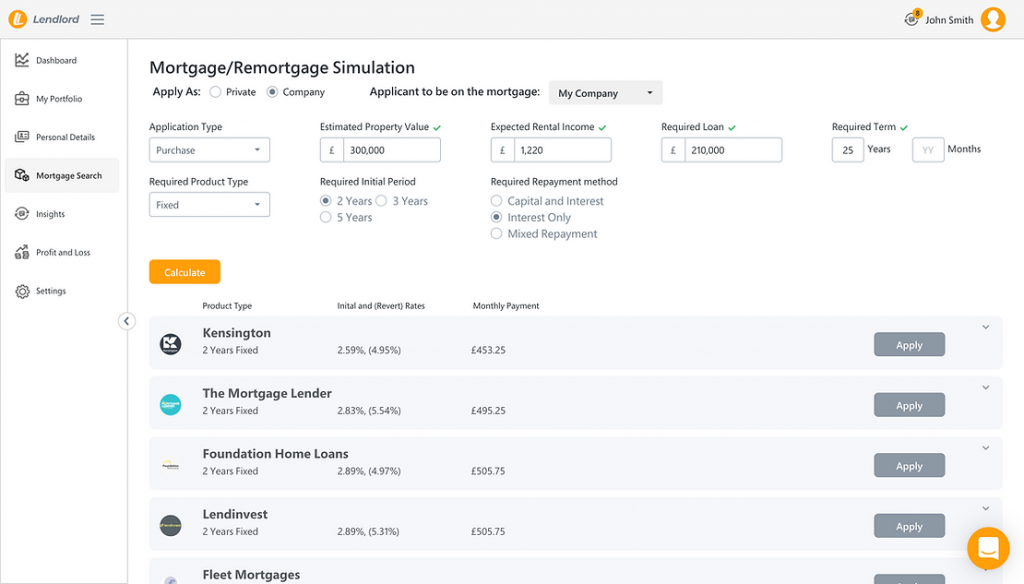

4. Click on “Mortgage Search” from the menu, enter the expected values of a prospect property and check which rates are available for you as a limited company (and which lenders the prospect property has met the criteria for):