We have just published a new article on the Property Reporter: “The seven metrics all landlords should be tracking”. In this post we would like to show you how you can start track those metrics using Lendlord.

Access to accurate information is important for managing your properties at any time, but in times of great uncertainty, when so many unknowns lie ahead, understanding the exact position of your portfolio can prove crucial.

After all, in a difficult environment, with potential pitfalls around every corner and opportunities fewer and farther between, the ability to make good decisions becomes more vital. And the best way to make good decisions, is with access to the right information.

So, with this in mind, what important metrics should you be tracking?

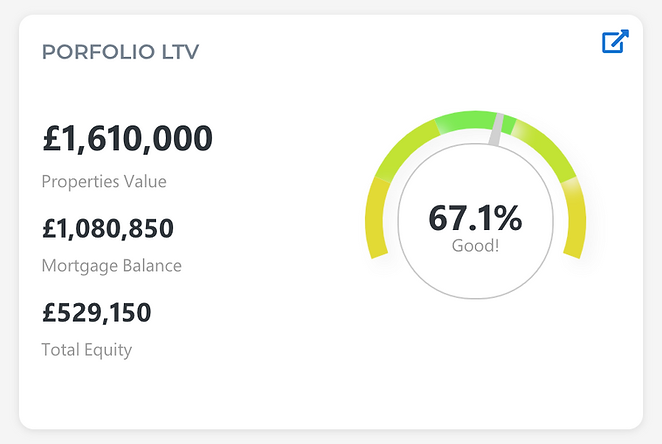

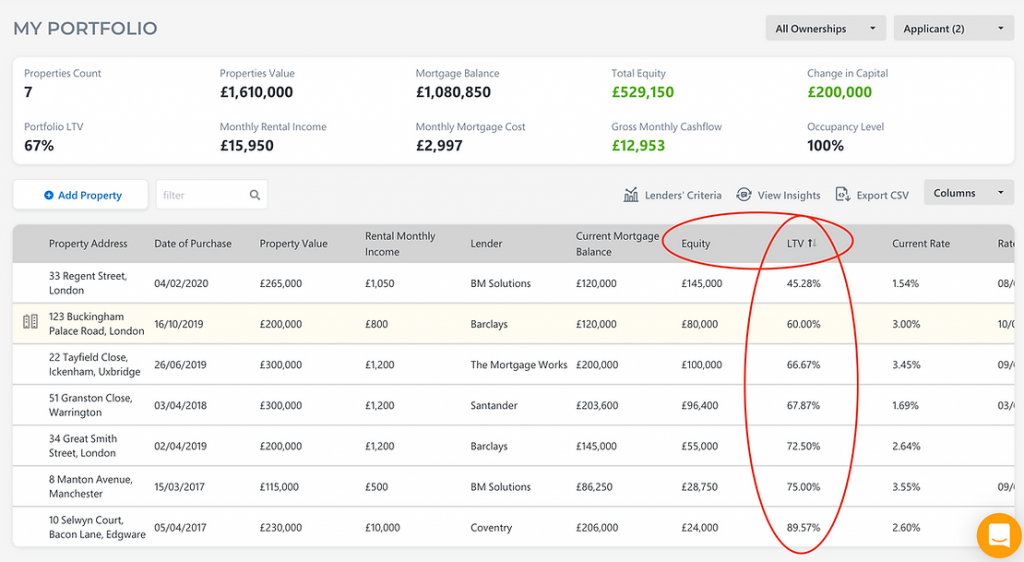

LTV

With up-to-date information on the LTV of your individual properties and of your portfolio, you will have a better idea of your current position and your options to refinance. Some lenders have restrictions on the overall LTV of a portfolio and criteria can change quickly in the current environment.

Portfolio Total Equity

How much equity do you have in your portfolio? Knowing the current estimated property value minus the current balance of mortgages and other loans, will give you a clearer idea of the choices you have, particularly if you are thinking of refinancing to capitalise on the stagnant property market and expand your portfolio.

How to track your LTV and Total Equity using Lendlord:

1. In your dashboard you can see the LTV widget that shoes your current portfolio LTV, how much you currently have in equity and how much is your entire mortgage balance:

2. In “My Portfolio” page, you can see 2 attributes “Equity” and “LTV” for each property. You can sort your portfolio table order by the “Equity” or “LTV” columns:

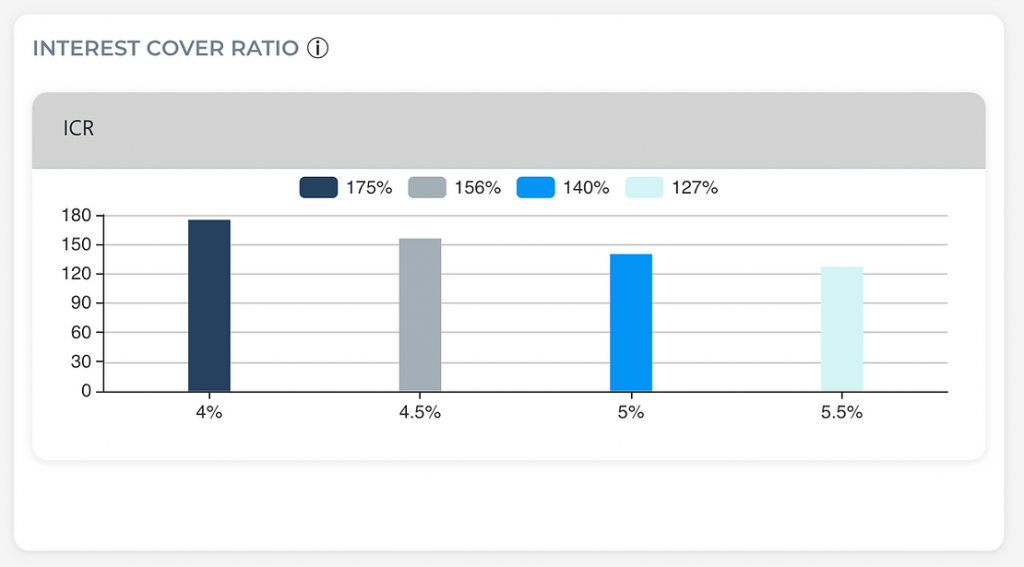

Portfolio Interest Cover Ratio

The Interest Cover Ratio (ICR) of your portfolio, based on your outgoing interest payments and incoming rental income, is used by lenders to determine the resilience of your portfolio to increases in interest rate and it can be a key determining factor in your ability to secure a new mortgage. BM Solutions, for example, carries out a stress test that requires rental income to cover at least 145% of mortgage interest payments at

5.50% across the portfolio. Understanding the position of your portfolio will help you to understand your options.

How to see your Portfolio ICR using Lendlord:

1. From My Portfolio page, click on “Lenders’ Criteria” (right above the portfolio table).

2. On the right side you will see your Portfolio ICR:

Rental Cover Ratio

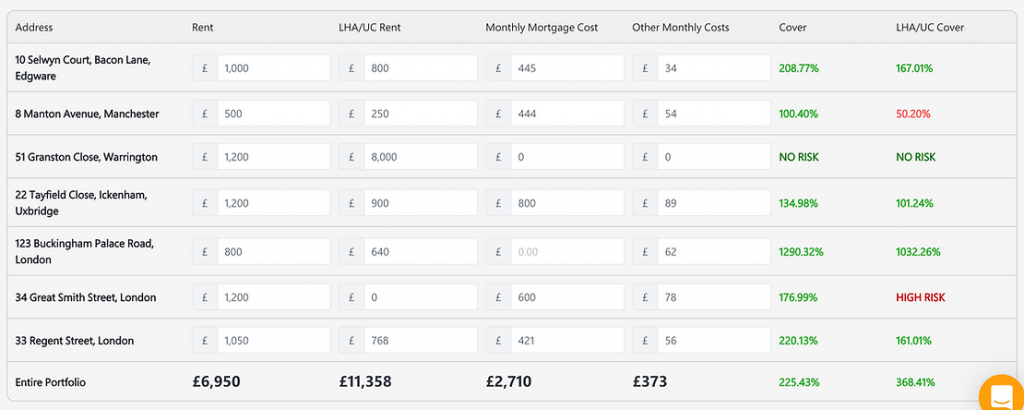

You should also stress test each property and the entire portfolio with your current interest rate and mortgage monthly cost, in case your tenants stop paying their rent or are only able to make payments based on Local Housing Authority rates or Universal Credit. This metric will help you understand your overall risk level on the entire portfolio level and how much runway you have if your tenants stop paying and is, needless to say, particularly important at the moment.

How to see what is your current Rental Cover Ratio using Lendlord:

1. It’s currently available from your dashboard. Click on: “Stress Test Your Portfolio”:

2. In the screen, you should put the amount you should expect to get in your worst case scenario and review your risk level:

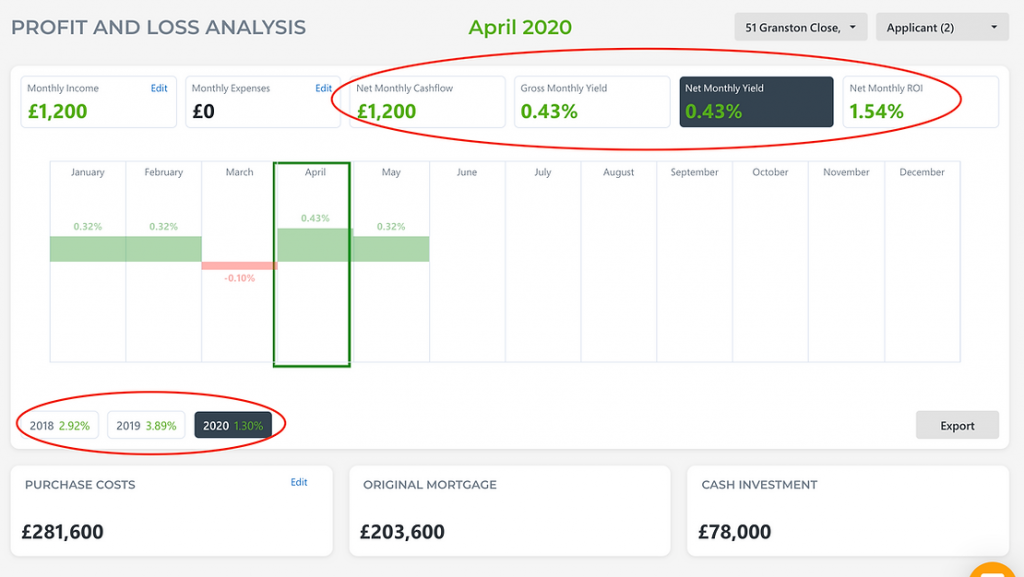

Net Cashflow

Your actual cashflow is based on the actual rental income minus the actual monthly expenses. Net cashflow is often different to gross cashflow, which is rental income minus fixed costs.

Yield

It is important to stay on top of the gross yield of your portfolio, which is the annual income generated by the assets divided by their price, and the net yield, which is the annual profit minus costs generated by the assets and divided by their price.

ROI

Possibly the most important metric of any investment is the ROI, or return on investment. This is the annual profit (income minus costs) generated by your portfolio, divided by the cash you have put in.

How to see your net cashflow, Gross/Net Yield and ROI using Lendlord:

1. Go to “Profit and Loss” page.

2. Make sure you tracked your purchase costs on each property and your monthly expenses.

3. You can review your monthly figures and your annual figures (below the main chart):