Stamp Duty Land Tax (SDLT) is a tax levied by the UK government on property and land transactions. It applies when purchasing property or land over a certain value in England and Northern Ireland. To determine what you might owe, you can use a stamp duty calculator to estimate the amount based on the property’s purchase price and current tax bands. The purpose of SDLT is to generate revenue for public services and regulate property market activity.

UK Stamp Duty Rates Visualization

UK Stamp Duty Rates Dashboard

Lendlord.io

Residential SDLT Rates

Standard residential SDLT rates across different property price bands:

0% up to £250,000, 5% from £250,001 to £925,000,

10% from £925,001 to £1.5 million, and 12% over £1.5 million.

First-Time Buyer Relief

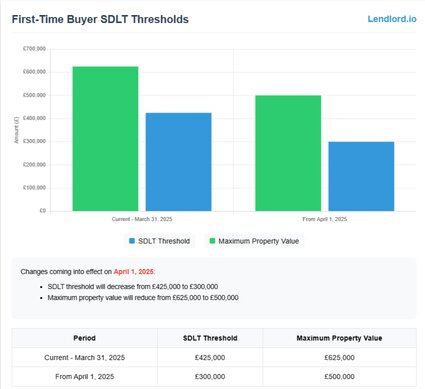

Comparison of First-Time Buyer relief thresholds before and after April 2025.

Current relief up to £425,000 (max property value £625,000) changing to

£300,000 (max property value £500,000).

Non-Residential SDLT Rates

Non-residential and mixed-use property SDLT rates:

0% up to £150,000, 2% from £150,001 to £250,000,

and 5% over £250,000.

SDLT Changes Timeline

Timeline showing key SDLT threshold changes coming into effect on April 1, 2025,

including the decrease in standard threshold from £250,000 to £125,000.

What’s in this blog post?

Current UK Stamp Duty Rates and Thresholds

Residential Property Rates

The SDLT rates for residential properties vary based on the property price and buyer type. The standard SDLT rate is tiered, meaning different portions of the property price fall into different tax bands:

Up to £250,000: 0% (No SDLT is payable)

£250,001 – £925,000: 5%

£925,001 – £1.5 million: 10%

Over £1.5 million: 12%

First-time buyers receive special relief, where they do not pay SDLT on the first £425,000 of the purchase price, provided the property is valued up to £625,000.

SDLT Rates Table

Stamp Duty Land Tax (SDLT) Rates

Lendlord.io

Property Price Band

Standard Rate

First-Time Buyer Rate

Up to £250,000

0%

0%

£250,001 - £425,000

5%

0%

£425,001 - £925,000

5%

5%

£925,001 - £1.5 million

10%

10%

Over £1.5 million

12%

12%

First-Time Buyer Relief: First-time buyers don't pay SDLT on the first £425,000

of the purchase price, provided the property is valued up to £625,000. Above £625,000,

standard rates apply to the entire purchase price.

Non-Residential and Mixed-Use Property Rates

Non-Residential SDLT Rates

Non-Residential SDLT Rates

Lendlord.io

These rates apply to non-residential and mixed-use properties. Mixed-use properties are those that have both residential and non-residential elements. The rate applied depends on the property purchase price and is calculated on a tiered basis.

Non-residential properties and mixed-use properties (those that have both residential and non-residential use) are taxed differently. The rates for these types of properties are:

Up to £150,000: 0%

£150,001 – £250,000: 2%

Over £250,000: 5%

Changes to UK Stamp Duty Rates and Thresholds Effective April 1, 2025

Reduction in SDLT Thresholds

On April 1, 2025, changes to SDLT thresholds will come into effect, impacting both residential and first-time buyers. The standard SDLT threshold will decrease from £250,000 to £125,000. This means that any property purchase over £125,000 will be subject to SDLT, leading to higher upfront costs for many buyers.

First-time buyers will also see a reduction in their relief threshold, from £425,000 to £300,000 for properties valued up to £500,000. This change aims to balance the housing market, but may also present challenges for first-time buyers facing increased costs.

Impact on Homebuyers

These changes will likely affect the affordability of properties, especially for first-time buyers and those purchasing in high-demand areas. First-time buyers may need to budget more for SDLT, and existing homeowners may see reduced flexibility in moving to larger properties.

For homebuyers, navigating the new thresholds means planning finances carefully and possibly seeking advice from property tax specialists. The government aims to ensure a fairer distribution of tax burdens, but market analysts have voiced concerns about the impact on the property market’s fluidity.

Calculating Your UK Stamp Duty Liability

Calculating SDLT liability is straightforward but requires an understanding of the relevant rates and thresholds. For residential properties, SDLT is calculated on the portion of the property price within each band. For example, if buying a property for £450,000, SDLT is applied as follows:

£250,000 at 0%: £0

£200,000 at 5%: £10,000

Total SDLT payable would be £10,000.

Buyers can use online SDLT calculators provided by websites like GOV.UK or Rightmove to estimate their liability quickly. Special considerations are necessary for additional properties, where an extra surcharge is applied.

UK Stamp Duty Surcharges for Additional Properties

If you are purchasing an additional property—such as a second home or buy-to-let investment—a surcharge is applied to the standard SDLT rates. Currently, the surcharge is 3%, but it recently increased to 5% as of October 31, 2024.

This means that an individual buying an additional property for £400,000 will pay an extra 5% SDLT on top of the standard rates. The surcharge is intended to manage housing supply and discourage speculative purchases that could otherwise make housing less affordable for first-time buyers.

Certain exemptions are available for buyers who sell their previous main residence within 36 months, allowing them to reclaim the surcharge. Understanding the nuances of these exemptions can save significant amounts of money for landlords and investors.

Regional Variations in UK Property Transaction Taxes

Scotland: Land and Buildings Transaction Tax (LBTT)

Scotland has its own property transaction tax called Land and Buildings Transaction Tax (LBTT), which differs from SDLT in both rates and thresholds. The LBTT applies to residential and non-residential properties, with different bands.

LBTT thresholds are generally more favorable for lower-value properties, benefiting first-time buyers in Scotland. Buyers should refer to Revenue Scotland for up-to-date rates and guidance.

Wales: Land Transaction Tax (LTT)

In Wales, the Land Transaction Tax (LTT) replaced SDLT in 2018. LTT is structured similarly but with different rates and thresholds, often resulting in lower tax obligations for lower-value properties. Buyers in Wales can find specific LTT information on the Welsh Revenue Authority website.

Frequently Asked Questions (FAQs) on UK Stamp Duty Rates and Thresholds

What is the current stamp duty threshold for first-time buyers?

The current SDLT threshold for first-time buyers is £425,000 for properties valued up to £625,000. From April 1, 2025, this threshold will be reduced to £300,000 for properties valued up to £500,000.

stamp duty threshold for first-time buyers

How will the stamp duty changes in April 2025 affect homebuyers?

The changes will result in higher SDLT liabilities for most buyers, particularly those purchasing properties over £125,000. First-time buyers will need to consider their budget more carefully due to the reduced relief threshold.

higher SDLT liabilities for most buyers

Are there any exemptions available for stamp duty?

Yes, certain exemptions are available, including first-time buyer relief, exemptions for properties under £125,000, and refunds for those who sell their main residence within three years of purchasing an additional property.

How does stamp duty differ between England, Scotland, and Wales?

England and Northern Ireland use SDLT, while Scotland uses LBTT and Wales uses LTT. Each tax has different rates and thresholds, which can affect the cost of buying property in these regions.

What are the penalties for late payment of stamp duty?

If Stamp Duty Land Tax (SDLT) is not paid within 14 days of the completion date of a property purchase, interest charges and possible fines will apply. As of 26 November 2024, the interest rate on late payments is 7.25%.

The late filing penalty increases to £200 for returns filed more than 3 months late. Early settlement of SDLT will help you avoid these charges.

What are the penalties for late payment of stamp duty?

Failure to pay SDLT within 14 days of the property purchase completion date results in interest and possible fines. It is essential to settle SDLT promptly to avoid additional costs.

Conclusion

Stamp Duty Land Tax (SDLT) is a significant factor in property purchases in England and Northern Ireland, affecting buyers differently based on property value, type, and buyer status. With upcoming changes in April 2025, understanding SDLT rates, thresholds, and exemptions is more crucial than ever.

Buyers should take advantage of online calculators to estimate SDLT liability and seek advice from professionals to ensure compliance and cost-effectiveness. Staying informed about regional variations like LBTT in Scotland and LTT in Wales will also help prospective homeowners plan better.

As the government continues to make adjustments, navigating SDLT will remain a key aspect of property transactions in the UK. Being prepared and understanding these changes will help buyers make informed decisions and minimize tax liabilities.

Sign Up for Free Today & Get 40% Off Lendlord Premium Plan!